Getting starting with the varPro R-package for model-independent variable selection in regression, classification, survival and unsupervised settings

Min Lu (luminwin@gmail.com)

Aster Shear (aster.shear@gmail.com)

Udaya B. Kogalur (ubk@kogalur.com)

Hemant Ishwaran

(hemant.ishwaran@gmail.com)

2025-04-22

getstarted.Rmd

Overview

VarPro is a novel method for variable selection based on rule-based

models. These include decision rules, decision trees, Bayesian Adaptive

Regression Trees (BART), Bayesian forests, and random forests. Such

rule-based procedures do not require predefined model specifications and

can accommodate a variety of outcome types, including regression,

classification, survival, and longitudinal data. The current

implementation of the VarPro software uses rules extracted from random

forests via the randomForestSRC package.

Traditional variable selection methods, such as permutation variable importance (VIMP) [1–3] and knockoffs [4], have known limitations. Both rely on generating artificial covariates, which can lead to unreliable results when these synthetic variables fail to reflect the structure of the original data.

VarPro takes a different approach. Rather than introducing artificial covariates, it constructs release rules that selectively relax variable constraints to evaluate how each variable influences the response. By working within local neighborhoods defined by observed data, VarPro avoids the pitfalls of synthetic variable generation and provides a robust, flexible framework for assessing variable importance. Like VIMP and knockoffs, it makes no assumptions about the conditional distribution of the response.

How VarPro Works

The VarPro algorithm proceeds in two main stages:

- Guided Tree Splitting

A forest of

ntreetrees is grown using guided splitting, where variables are selected with probability based on their split-weights.This process encourages rules that are more likely to involve influential variables.

- Rule Harvesting

A random subset of

max.treetrees is selected.From each of these trees, a subset of

max.rules.treebranches (rules) is sampled.

- VarPro Importance

The importance of a variable is calculated by comparing local estimators of a target function within a rule-defined region and a released version of that region (for example, in regression, , so , and in classification, for class , so ).

For each rule, VarPro computes the sample average of the outcome in the region defined by the rule, and compares it to the average in a released region—one where constraints on the variable(s) being tested are removed.

-

The importance score for a variable (or set of variables) is the absolute difference between these two local averages:

where:

- is the average of in the original region,

- is the average in the released region with variable(s) in unconstrained.

This process is repeated across multiple rules, and the final VarPro importance is a weighted average.

Because VarPro uses only observed data—no artificial permutations or synthetic features—it avoids biases that affect other variable importance methods such as permutation importance and knockoffs.

The current version of the software applies a modification where the Importance is locally standardized. This is now used for the default setting.

VarPro is applicable to:

Regression

Multivariate regression

Multiclass classification

Survival analysis

A new mode now handles unsupervised data

Split-Weights

Guided splitting depends on split-weights, which determine how often a variable is chosen for splitting. By default, these weights are derived using a combination of lasso regression, shallow trees, and in some instances, permutation importance.

The split-weight of a variable is defined as the absolute standardized lasso coefficient, multiplied by its frequency in a forest of shallow trees.

If the sample size and number of features are moderate, split-weights may instead rely on permutation importance.

To use lasso effectively, all variables (including factors) are converted to real-valued features via one-hot encoding.

You can customize how

split-weights are computed using the

split.weight.method option:

“lasso” – Use only lasso coefficients.

“lasso tree” – Combine lasso with tree-based importance.

“lasso vimp” – Combine lasso with permutation importance.

Variable Selection and Thresholding

Variables are ranked based on their VarPro importance scores. Larger values indicate more influential features. You can use cross-validation) to select a threshold for identifying relevant variables.

Performance and Customization

For faster runtimes, use fewer trees (

ntree) and increase the minimum terminal node size (nodesize).Additional tuning options are available. See the examples section for more details.

Handling Class Imbalance

For binary classification tasks with class imbalance, VarPro

automatically uses Random Forest Quantile Classification (RFQ) [5, 6]. This behavior can be overridden with the

use.rfq option.

Quick Start

Quick Installation

Like many other R packages, the simplest way to obtain

randomForestSRC is to install it directly from CRAN or

Github via typing the following command in R console:

# install.packages("devtools")

devtools::install_github("kogalur/varPro")

# another way

install.packages("varPro", repos = "https://cran.us.r-project.org")A Quick Example of Regression

library(varPro)

## check the data

data(Boston, package = "MASS")

head(Boston)

> crim zn indus chas nox rm age dis rad tax ptratio black lstat medv

> 1 0.00632 18 2.31 0 0.538 6.575 65.2 4.0900 1 296 15.3 396.90 4.98 24.0

> 2 0.02731 0 7.07 0 0.469 6.421 78.9 4.9671 2 242 17.8 396.90 9.14 21.6

> 3 0.02729 0 7.07 0 0.469 7.185 61.1 4.9671 2 242 17.8 392.83 4.03 34.7

> 4 0.03237 0 2.18 0 0.458 6.998 45.8 6.0622 3 222 18.7 394.63 2.94 33.4

> 5 0.06905 0 2.18 0 0.458 7.147 54.2 6.0622 3 222 18.7 396.90 5.33 36.2

> 6 0.02985 0 2.18 0 0.458 6.430 58.7 6.0622 3 222 18.7 394.12 5.21 28.7

## call varpro

o <- varpro(medv ~ ., data = Boston)

## extract and print importance values

imp <- importance(o)

print(imp)

> z

> rm 2.8020301

> lstat 2.4851461

> nox 1.7625229

> ptratio 1.6138725

> dis 1.2464620

> crim 1.1134819

> b 0.8257784

> tax 0.1076922

> indus 0.0581391

> age 0.0000000

> chas 0.0000000

> rad 0.0000000

## plot importance values

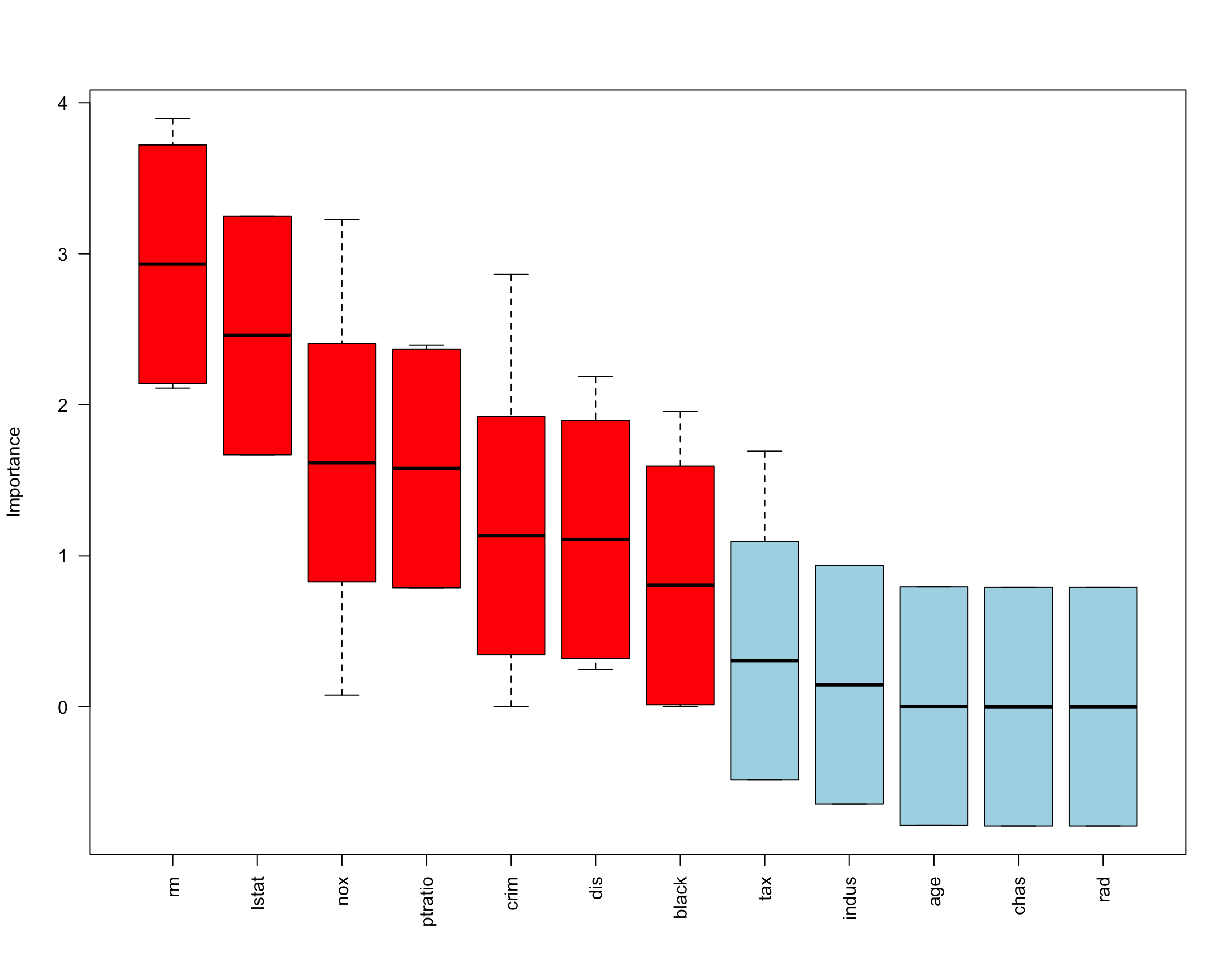

importance(o, plot.it = TRUE)

In the

above output, print(imp) display the VarPro importance.

In the above figure, important variables are marked in red color while noise variables are marked in blue color.

Note that not all of the variables will be listed nor plotted in the output since the varPro algorithm prefilters noise variables before calculating the importance values.

Cross-validated Cutoff Value for VarPro

To tune the cutoff value of VarPro for the final variable selection decision, our package also provides a function to fit a random forest model in a forward fitting fashion where variables were added in to the model according to a grid of cutoff values. The optimal subset of variables is defined by the random forest model with the smallest out-of-bag error.

o <- cv.varpro(medv ~ ., data = Boston)

print(o)

$imp

variable z

1 lstat 3.6781189

2 rm 3.4421867

3 ptratio 2.0686261

4 nox 1.2541217

5 crim 1.2162352

6 dis 1.0108895

7 black 0.4816799

$imp.conserve

variable z

1 lstat 3.678119

2 rm 3.442187

3 ptratio 2.068626

4 nox 1.254122

$imp.liberal

variable z

1 lstat 3.6781189

2 rm 3.4421867

3 ptratio 2.0686261

4 nox 1.2541217

5 crim 1.2162352

6 dis 1.0108895

7 black 0.4816799

$err

zcut nvar err sd

[1,] 0.1000000 7 0.2039396 0.008710617

[2,] 0.4877551 6 0.2162618 0.011050992

[3,] 1.0306122 5 0.2155826 0.009447152

[4,] 1.2244898 4 0.2052468 0.013659195

[5,] 1.2632653 3 0.2399562 0.014592443

$zcut

[1] 0.1

$zcut.conserve

[1] 1.22449

$zcut.liberal

[1] 0.1In the above output, lines for $imp display the final

list of variables that minimize out-of-sample error rate of a random

forest, where the error rates were listed in lines for

$error. Its cutoff value for the VarPro standardized

importance is listed in lines for $zcut. Lines for

$imp.conserve and $imp.liberal display a

“conservative” and “liberal” list of variables returned using a one

standard deviation rule. The conservative list comprises variables using

the largest cutoff with error rate within one standard deviation from

the optimal cutoff error rate, whereas the liberal list uses the

smallest cutoff value with error rate within one standard deviation of

the optimal cutoff error rate.

More examples for regression, classification, survival and unsupervised problems

Regression with hot-encoding

## load the data

data(BostonHousing, package = "mlbench")

head(BostonHousing)

crim zn indus chas nox rm age dis rad tax ptratio b lstat medv

1 0.00632 18 2.31 0 0.538 6.575 65.2 4.0900 1 296 15.3 396.90 4.98 24.0

2 0.02731 0 7.07 0 0.469 6.421 78.9 4.9671 2 242 17.8 396.90 9.14 21.6

3 0.02729 0 7.07 0 0.469 7.185 61.1 4.9671 2 242 17.8 392.83 4.03 34.7

4 0.03237 0 2.18 0 0.458 6.998 45.8 6.0622 3 222 18.7 394.63 2.94 33.4

5 0.06905 0 2.18 0 0.458 7.147 54.2 6.0622 3 222 18.7 396.90 5.33 36.2

6 0.02985 0 2.18 0 0.458 6.430 58.7 6.0622 3 222 18.7 394.12 5.21 28.7

## convert some of the features to factors

Boston <- BostonHousing

Boston$zn <- factor(Boston$zn)

Boston$chas <- factor(Boston$chas)

Boston$lstat <- factor(round(0.2 * Boston$lstat))

Boston$nox <- factor(round(20 * Boston$nox))

Boston$rm <- factor(round(Boston$rm))

## call varpro and print the importance

print(importance(o <- varpro(medv~., Boston)))

z

rm8 5.47876912

lstat1 2.84240815

rm6 2.62702059

lstat2 1.96640588

rm7 1.93009100

crim 1.91978125

nox14 1.90744534

ptratio 1.48896289

tax 1.04818974

nox13 0.99046707

b 0.73989233

indus 0.68380574

lstat5 0.66820269

dis 0.59586207

age 0.44459518

nox10 0.28498938

lstat0 0.27933331

lstat4 0.24870583

lstat6 0.04865196

chas 0.01651904

nox11 0.00000000

nox12 0.00000000

nox17 0.00000000

rad 0.00000000

rm9 0.00000000

zn90 0.00000000

## get top variables

get.topvars(o)

[1] "rm8" "rm6" "lstat1" "nox14" "crim" "lstat2" "rm7" "ptratio" "nox13"

[10] "tax" "dis" "b" "indus" "age" "lstat5" "lstat0" "nox10" "lstat4"

[19] "lstat6" "chas" "nox11" "nox12" "nox17" "rad" "rm9" "zn90"

## map importance values back to original features

print(get.orgvimp(o))

variable z

6 rm 5.6336672

13 lstat 2.7783778

5 nox 2.0679178

1 crim 1.9483674

11 ptratio 1.5227539

10 tax 1.0942222

12 b 0.7622109

8 dis 0.6932214

3 indus 0.6729344

7 age 0.4207372

2 zn 0.0000000

4 chas 0.0000000

9 rad 0.0000000

## same as above ... but for all variables

print(get.orgvimp(o, pretty = FALSE))

crim zn indus chas nox rm age dis rad tax

1.8527969 0.0000000 0.6973291 0.0000000 1.7652739 5.6260698 0.5494061 1.0707970 0.0000000 1.1394922

ptratio b lstat

1.4486139 0.9302271 2.7298017 Multivariate regression

data(BostonHousing, package = "mlbench")

## using cbind multivariate formula call

importance(varpro(cbind(lstat, nox) ~., BostonHousing))

[[1]]

z

medv 2.8373757

rm 2.2395107

indus 1.4832981

age 1.4434773

dis 1.1467323

crim 0.8905107

tax 0.2178625

b 0.0000000

ptratio 0.0000000

rad 0.0000000

zn 0.0000000

[[2]]

z

indus 3.6984597

dis 3.1230747

crim 2.1167525

age 1.7821251

medv 1.3248673

rm 1.0124103

tax 0.7094792

b 0.0000000

ptratio 0.0000000

rad 0.0000000

zn 0.0000000

## equivalent as using rfsrc multivariate formula call

# importance(varpro(Multivar(lstat, nox) ~., BostonHousing))Classification

# use the iris data as an example. Check the data:

head(iris)

Sepal.Length Sepal.Width Petal.Length Petal.Width Species

1 5.1 3.5 1.4 0.2 setosa

2 4.9 3.0 1.4 0.2 setosa

3 4.7 3.2 1.3 0.2 setosa

4 4.6 3.1 1.5 0.2 setosa

5 5.0 3.6 1.4 0.2 setosa

6 5.4 3.9 1.7 0.4 setosa

## apply varpro to the iris data

o <- varpro(Species ~ ., iris)

## call the importance function and print the results

print(importance(o))

$unconditional

z

Petal.Length 3.292862

Petal.Width 3.252240

Sepal.Width 0.000000

$conditional.z

setosa versicolor virginica

Petal.Length 0.2048927 5.536114 1.794192

Petal.Width 4.9433575 6.056593 3.723534

Sepal.Width 0.0000000 0.000000 0.000000Survival

data(pbc, package = "randomForestSRC")

head(pbc)

days status treatment age sex ascites hepatom spiders edema bili chol albumin copper alk sgot

1 400 1 1 21464 1 1 1 1 1.0 14.5 261 2.60 156 1718.0 137.95

2 4500 0 1 20617 1 0 1 1 0.0 1.1 302 4.14 54 7394.8 113.52

3 1012 1 1 25594 0 0 0 0 0.5 1.4 176 3.48 210 516.0 96.10

4 1925 1 1 19994 1 0 1 1 0.5 1.8 244 2.54 64 6121.8 60.63

5 1504 0 2 13918 1 0 1 1 0.0 3.4 279 3.53 143 671.0 113.15

6 2503 1 2 24201 1 0 1 0 0.0 0.8 248 3.98 50 944.0 93.00

trig platelet prothrombin stage

1 172 190 12.2 4

2 88 221 10.6 3

3 55 151 12.0 4

4 92 183 10.3 4

5 72 136 10.9 3

6 63 NA 11.0 3

o <- varpro(Surv(days, status)~., pbc)

print(importance(o))

z

bili 2.4223890

edema 1.6002777

copper 1.2203896

ascites 1.0023466

albumin 0.9590398

prothrombin 0.8745652

age 0.6094406

stage 0.3043256

chol 0.0000000

hepatom 0.0000000

sgot 0.0000000See more survival problems.

Unsupervised clustering

data(BostonHousing, package = "mlbench")

## default call

o <- uvarpro(BostonHousing)

print(importance(o))

mean std z

indus 0.5889298 0.3465154 1.6995778

nox 0.5324178 0.3993524 1.3332031

medv 0.4519824 0.4315267 1.0474030

tax 0.3339766 0.3590255 0.9302308

rad 0.3264583 0.3538616 0.9225594

zn 0.3686787 0.4057892 0.9085474

crim 0.3380561 0.4019666 0.8410055

lstat 0.3248712 0.4206612 0.7722872

dis 0.2526544 0.3832465 0.6592476

ptratio 0.1881419 0.3276218 0.5742654

age 0.1946974 0.3572511 0.5449876

rm 0.1481955 0.3230311 0.4587656

b 0.0000000 0.0000000 NaN

chas 0.0000000 0.0000000 NaNSee more unsupervised problems.

Different split-weight methods

We can use different split-weight methods:

## ----------------------------------------------------------------------

## high dimensional survival example using different split-weight methods

## ----------------------------------------------------------------------

data(vdv, package = "randomForestSRC")

vdv[1:5,1:17]

Time Censoring AA555029_RC AA598803_RC AB002301 AB002308 AB002331 AB002351 AB002445

1 12.53 0 -0.5049331 -0.2425008 -0.199315682 0.90024251 0.6311663 -0.601269 0.44181645

2 6.44 0 -0.5879813 0.4384945 -0.621200562 0.09301399 0.9500715 -1.484902 0.21924725

3 10.66 0 -0.3521244 -0.2258911 0.006643856 0.13952097 -0.7275022 -1.043085 -0.27572003

4 13.00 0 -0.4750357 0.5016111 -0.671029449 0.76404345 -0.9234960 -1.926718 -0.01993157

5 11.98 0 -0.1660964 0.1361991 0.989934564 0.62452251 0.9168522 -1.455004 0.07972627

AB002448 AB004064 AB004857 AB006625 AB006628 AB006746 AB007458 AB007855

1 -0.26575425 -2.80370736 0.1328771 -1.1427432 -0.52818656 -0.97000301 0.32222703 0.41856295

2 0.14616483 0.08637013 0.5913032 1.1859283 -0.70424873 -0.62120056 0.33883667 0.05979471

3 -0.49496728 0.56140584 0.7108926 1.2424011 -0.77068734 1.12613368 -0.38534367 -0.23253496

4 0.09301399 0.41524100 0.2425008 -0.9002425 0.07972627 -0.43517259 0.05315085 -1.56795001

5 0.77733117 0.19267184 -0.3720559 -0.9700030 -0.41856295 -0.07640435 -0.20263761 0.54147428

f <- as.formula(Surv(Time, Censoring)~.)

## lasso only

print(importance(varpro(f, vdv, split.weight.method = "lasso")))

z

Contig28552_RC 1.4208629

NM_020974 1.0405454

Contig47405_RC 0.6928171

## lasso and vimp

print(importance(varpro(f, vdv, split.weight.method = "lasso vimp")))

z

NM_020974 0.9678159

Contig28552_RC 0.9466678

U45975 0.6766980

Contig43983_RC 0.5508783

Contig47405_RC 0.4033919

NM_014181 0.2864786

AB020689 0.0000000

## lasso, vimp and shallow trees

print(importance(varpro(f, vdv, split.weight.method = "lasso vimp tree")))

z

NM_020974 1.1038727

Contig28552_RC 0.9501651

Contig43983_RC 0.7836134

Contig47405_RC 0.5493373

AB020689 0.3757536

U45975 0.3738694

Contig25290_RC 0.3589115

Contig55574_RC 0.0000000

NM_003108 0.0000000

NM_006681 0.0000000

NM_014181 0.0000000Customized split-weights

## load the data

data(BostonHousing, package = "mlbench")

## make some features into factors

Boston <- BostonHousing

Boston$zn <- factor(Boston$zn)

Boston$chas <- factor(Boston$chas)

Boston$lstat <- factor(round(0.2 * Boston$lstat))

Boston$nox <- factor(round(20 * Boston$nox))

Boston$rm <- factor(round(Boston$rm))

## get default custom split-weights: a named real vector

swt <- varPro:::get.splitweight.custom(medv~., Boston)

swt

crim indus age dis rad tax ptratio b zn0 zn12.5 zn17.5 zn18

1 1 1 1 1 1 1 1 1 1 1 1

zn20 zn21 zn22 zn25 zn28 zn30 zn33 zn34 zn35 zn40 zn45 zn52.5

1 1 1 1 1 1 1 1 1 1 1 1

zn55 zn60 zn70 zn75 zn80 zn82.5 zn85 zn90 zn95 zn100 chas nox8

1 1 1 1 1 1 1 1 1 1 1 1

nox9 nox10 nox11 nox12 nox13 nox14 nox15 nox17 rm4 rm5 rm6 rm7

1 1 1 1 1 1 1 1 1 1 1 1

rm8 rm9 lstat0 lstat1 lstat2 lstat3 lstat4 lstat5 lstat6 lstat7 lstat8

1 1 1 1 1 1 1 1 1 1 1

## define custom splits weight

swt <- swt[grepl("crim", names(swt)) |

grepl("zn", names(swt)) |

grepl("nox", names(swt)) |

grepl("rm", names(swt)) |

grepl("lstat", names(swt))]

swt[grepl("nox", names(swt))] <- 4

swt[grepl("lstat", names(swt))] <- 4

swt <- c(swt, strange=99999)

cat("custom split-weight\n")

print(swt)

crim indus age dis rad tax ptratio b zn0 zn12.5 zn17.5 zn18

1 1 1 1 1 1 1 1 1 1 1 1

zn20 zn21 zn22 zn25 zn28 zn30 zn33 zn34 zn35 zn40 zn45 zn52.5

1 1 1 1 1 1 1 1 1 1 1 1

zn55 zn60 zn70 zn75 zn80 zn82.5 zn85 zn90 zn95 zn100 chas nox8

1 1 1 1 1 1 1 1 1 1 1 4

nox9 nox10 nox11 nox12 nox13 nox14 nox15 nox17 rm4 rm5 rm6 rm7

4 4 4 4 4 4 4 4 1 1 1 1

rm8 rm9 lstat0 lstat1 lstat2 lstat3 lstat4 lstat5 lstat6 lstat7 lstat8 strange

1 1 4 4 4 4 4 4 4 4 4 99999

## call varpro with the custom split-weights

o <- varpro(medv~.,Boston,split.weight.custom=swt,verbose=TRUE,sparse=FALSE)

cat("varpro result\n")

print(importance(o))

z

lstat1 3.80058227

nox14 2.52599762

lstat2 2.40081592

nox13 2.26405255

lstat3 2.20891414

nox10 1.57659854

lstat5 1.53197178

crim 1.23040167

lstat0 1.21195016

nox11 1.14235212

lstat4 0.95613610

nox12 0.93286170

lstat6 0.76143191

nox9 0.56287351

nox8 0.47674733

zn20 0.45050785

zn0 0.40524283

nox15 0.24961443

nox17 0.20264288

zn25 0.17448268

zn22 0.02993067

lstat7 0.00000000

zn12.5 0.00000000

zn21 0.00000000

zn28 0.00000000

zn30 0.00000000

zn33 0.00000000

Cite this vignette as

M. Lu, A. Shear, U. B.

Kogalur, and H. Ishwaran. 2025. “varPro: getting started with varPro

vignette.” https://www.varprotools.org/articles/getstarted.html.

@misc{LuGettingStartedvarpro,

author = "Min Lu and Aster Shear and Udaya B. Kogalur and Hemant Ishwaran",

title = {{varPro}: getting started with {varPro} vignette},

year = {2025},

url = {http://www.varprotools.org/articles/getstarted.html},

howpublished = "\url{http://www.varprotools.org/articles/getstarted.html}",

note = "[accessed date]"

}