isopro to Identify Anomalous Data

Min Lu (luminwin@gmail.com)

Aster Shear (aster.shear@gmail.com)

Udaya B. Kogalur (ubk@kogalur.com)

Hemant Ishwaran

(hemant.ishwaran@gmail.com)

2025-04-29

The isopro function implements Isolation Forests (Liu et al., 2008) [1], a random forest-based technique designed for anomaly detection.

Unlike traditional methods, Isolation Forests use randomly constructed trees and leverage the concept of early isolation: rare or anomalous observations tend to split away from the rest of the data quickly under random partitioning.

How It Works

Trees are built using pure random splitting.

Each tree is trained on a small subsample of the data—typically much smaller than the 63.2% subsample rate used in traditional random forests.

The key idea: anomalous observations isolate faster, meaning they appear in terminal nodes at shallower depths.

The depth of an observation (i.e., number of splits before reaching a terminal node) becomes a natural anomaly score—shallower = more anomalous.

How to Use isopro

There are three main ways to run isopro:

- Unsupervised Analysis (most common)

Use the

dataargument only.Set the

methodoption to control how trees are built ("rnd", "unsupv", or "auto").

- Supervised Analysis (less common)

Provide both a

formulaand adataset.In this case, the analysis is supervised and the

methodoption is ignored.

- Using a VarPro Object (advanced)

Pass a fitted VarPro object directly.

This applies isolation forests to the dimension-reduced feature space produced by VarPro (e.g., from a previous

method = "unsupv"run).This is similar to the unsupervised mode but benefits from prior dimensionality reduction.

Choosing a Method

The method option determines how trees are

constructed:

-

“rnd” (pure random splitting):

Fastest method

Often effective, but not always optimal

-

“unsupv” (unsupervised tree splitting):

A balance of speed and structure

Works well in many cases

-

“auto” (auto-encoder splitting):

Most powerful, but slowest

Best suited for low-dimensional problems

We recommend experimenting with different methods, especially if your data has unique structure or high-dimensional features. See the simulation example below:

R Examples

## monte carlo parameters

nrep <- 25

n <- 1000

## simulation function

twodimsim <- function(n=1000) {

cluster1 <- data.frame(

x = rnorm(n, -1, .4),

y = rnorm(n, -1, .2)

)

cluster2 <- data.frame(

x = rnorm(n, +1, .2),

y = rnorm(n, +1, .4)

)

outlier <- data.frame(

x = -1,

y = 1

)

x <- data.frame(rbind(cluster1, cluster2, outlier))

is.outlier <- c(rep(FALSE, 2 * n), TRUE)

list(x=x, is.outlier=is.outlier)

}

## monte carlo loop

hbad <- do.call(rbind, lapply(1:nrep, function(b) {

cat("iteration:", b, "\n")

## draw the data

simO <- twodimsim(n)

x <- simO$x

is.outlier <- simO$is.outlier

## iso pro calls

i.rnd <- isopro(data=x, method = "rnd")

i.uns <- isopro(data=x, method = "unsupv")

i.aut <- isopro(data=x, method = "auto")

## save results

c(tail(i.rnd$howbad,1),

tail(i.uns$howbad,1),

tail(i.aut$howbad,1))

}))

## compare performance

colnames(hbad) <- c("rnd", "unsupv", "auto")

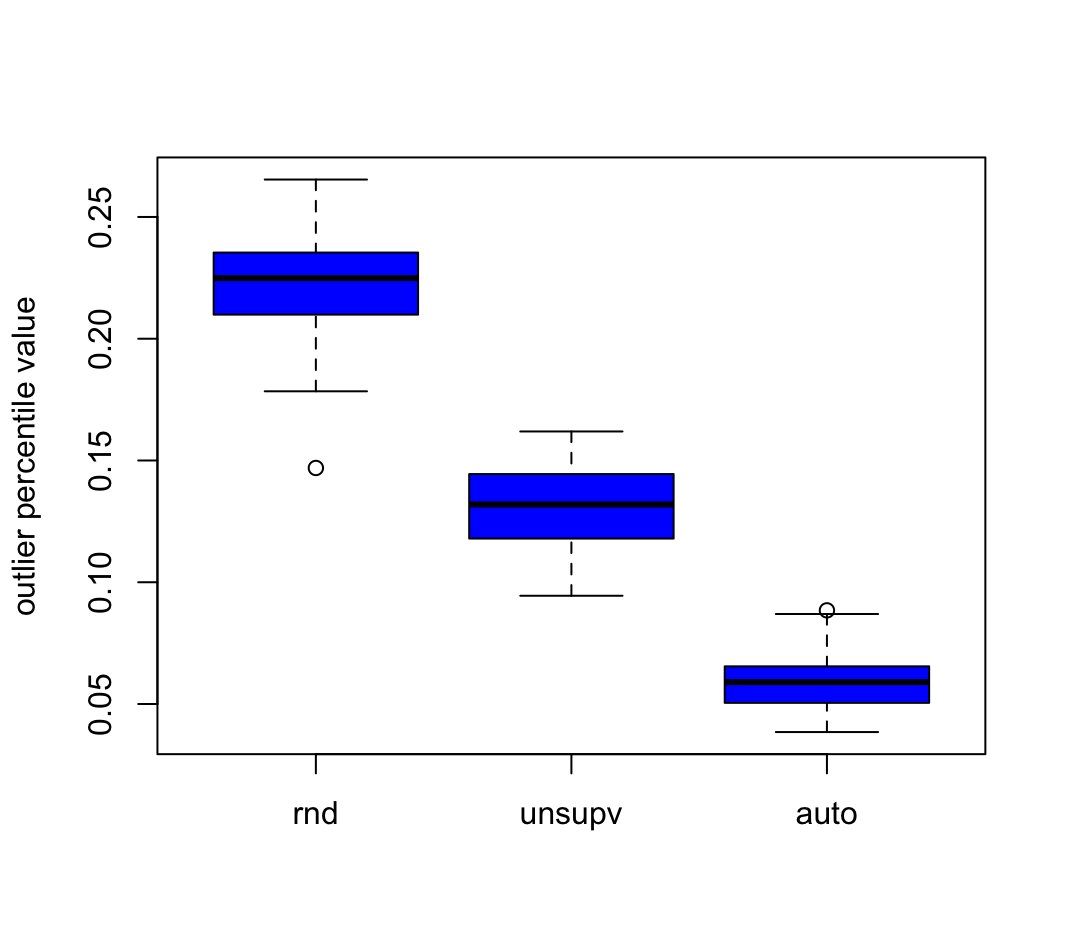

print(summary(hbad))

rnd unsupv auto

Min. :0.1469 Min. :0.09445 Min. :0.03848

1st Qu.:0.2099 1st Qu.:0.11794 1st Qu.:0.05047

Median :0.2249 Median :0.13193 Median :0.05897

Mean :0.2218 Mean :0.13049 Mean :0.05955

3rd Qu.:0.2354 3rd Qu.:0.14443 3rd Qu.:0.06547

Max. :0.2654 Max. :0.16192 Max. :0.08846

boxplot(hbad,col="blue",ylab="outlier percentile value")

Regression problem

data(BostonHousing, package = "mlbench")

## call varpro first and then isopro

o <- varpro(medv~., BostonHousing)

o.iso <- isopro(o)

## identify data with extreme percentiles

print(BostonHousing[o.iso$howbad <= quantile(o.iso$howbad, .01),])

crim zn indus chas nox rm age dis rad tax ptratio b lstat medv

143 3.32105 0 19.58 1 0.871 5.403 100.0 1.3216 5 403 14.7 396.90 26.82 13.4

145 2.77974 0 19.58 0 0.871 4.903 97.8 1.3459 5 403 14.7 396.90 29.29 11.8

481 5.82401 0 18.10 0 0.532 6.242 64.7 3.4242 24 666 20.2 396.90 10.74 23.0

482 5.70818 0 18.10 0 0.532 6.750 74.9 3.3317 24 666 20.2 393.07 7.74 23.7

483 5.73116 0 18.10 0 0.532 7.061 77.0 3.4106 24 666 20.2 395.28 7.01 25.0

484 2.81838 0 18.10 0 0.532 5.762 40.3 4.0983 24 666 20.2 392.92 10.42 21.8Supervised isopro analysis - direct call using formula/data

data(BostonHousing, package = "mlbench")

## direct approach uses formula and data options

o.iso <- isopro(formula=medv~., data=BostonHousing)

## identify data with extreme percentiles

print(BostonHousing[o.iso$howbad <= quantile(o.iso$howbad, .01),])

crim zn indus chas nox rm age dis rad tax ptratio b lstat medv

162 1.46336 0 19.58 0 0.605 7.489 90.8 1.9709 5 403 14.7 374.43 1.73 50

163 1.83377 0 19.58 1 0.605 7.802 98.2 2.0407 5 403 14.7 389.61 1.92 50

164 1.51902 0 19.58 1 0.605 8.375 93.9 2.1620 5 403 14.7 388.45 3.32 50

167 2.01019 0 19.58 0 0.605 7.929 96.2 2.0459 5 403 14.7 369.30 3.70 50

284 0.01501 90 1.21 1 0.401 7.923 24.8 5.8850 1 198 13.6 395.52 3.16 50

371 6.53876 0 18.10 1 0.631 7.016 97.5 1.2024 24 666 20.2 392.05 2.96 50Unsupervised problem

## load data, make three of the classes into outliers

data(Satellite, package = "mlbench")

is.outlier <- is.element(Satellite$classes,

c("damp grey soil", "cotton crop", "vegetation stubble"))

## remove class labels, make unsupervised data

x <- Satellite[, names(Satellite)[names(Satellite) != "classes"]]

## isopro calls

i.rnd <- isopro(data=x, method = "rnd", sampsize=32)

i.uns <- isopro(data=x, method = "unsupv", sampsize=32)

i.aut <- isopro(data=x, method = "auto", sampsize=32)

## AUC and precision recall (computed using true class label information)

perf <- cbind(get.iso.performance(is.outlier,i.rnd$howbad),

get.iso.performance(is.outlier,i.uns$howbad),

get.iso.performance(is.outlier,i.aut$howbad))

colnames(perf) <- c("rnd", "unsupv", "auto")

print(perf)

rnd unsupv auto

auc 0.5940483 0.8233815 0.7266512

pr.auc 0.5268934 0.7726910 0.6562785

Cite this vignette as

M. Lu, A. Shear, U. B.

Kogalur, and H. Ishwaran. 2025. “isopro: identifying anomalous data

vignette.” http://www.varprotools.org/articles/isopro.html.

@misc{LuIsopro,

author = "Min Lu and Aster Shear and Udaya B. Kogalur and Hemant Ishwaran",

title = {{isopro}: Identifying Anomalous Data vignette},

year = {2025},

url = {http://www.varprotools.org/articles/isopro.html},

howpublished = "\url{http://www.varprotools.org/articles/isopro.html}",

note = "[accessed date]"

}