varPro for unsupervised problems

Min Lu (luminwin@gmail.com)

Lili Zhou (lxz516@miami.edu)

Aster Shear (aster.shear@gmail.com)

Udaya B. Kogalur (ubk@kogalur.com)

Hemant Ishwaran

(hemant.ishwaran@gmail.com)

2026-04-01

unsupervise.Rmd

Introduction

Unsupervised feature selection plays a vital role in high-dimensional data analysis, especially in fields such as bioinformatics, imaging, and text mining, where labeled outcomes are often unavailable or costly to obtain. In the absence of supervision, identifying informative variables becomes a fundamentally different and more challenging task: without a response to guide selection, variable importance must be inferred from the intrinsic structure of the data itself.

We address this challenge by extending the Variable Priority (VarPro) framework, originally developed for supervised learning, to the unsupervised domain. The resulting approach, known as Unsupervised Variable Priority (UVarPro), reframes feature selection as a sequence of localized two-class classification tasks, where the class labels arise from rule-based data partitions and their complement regions. This transformation introduces a layer of supervision grounded in statistical dependence and Bayes’ theorem, enabling principled importance estimation without labeled data.

Unlike purely heuristic approaches based on variance or clustering alignment, UVarPro draws from a more formal notion of informativeness: a variable is considered a signal if it explains the joint structure of the data and contributes to dependencies among features. This aligns with the concept of a Markov blanket in graphical models, where a minimal set of variables renders others conditionally independent. By leveraging this principle, UVarPro selects variables that preserve essential structure while filtering out noise.

UVarPro is implemented by the uvarpro function which

provides multiple strategies for unsupervised forest construction,

controlled by the method argument:

method = "auto"(default): Constructs a random forest autoencoder by regressing selected variables against themselves. This specialized multivariate forest effectively learns the internal structure of the data but may be slower on large datasets.method = "unsupv": Builds forests using standard unsupervised random forest techniques that do not rely on any response variable. This approach offers a good balance between scalability and structural fidelity.method = "rnd": Constructs forests using pure random splitting, independent of data-driven criteria. While this sacrifices structural precision, it offers the fastest performance and is useful for extremely large datasets.

Feature importance in uvarpro is quantified using an

entropy-based criterion derived from the overall variability explained

by each variable. Users may also supply custom entropy functions to

tailor the importance scoring mechanism to specific applications. See

the examples below.

For further details, see Zhou, Lu and Ishwaran (2025). Variable Priority for Unsupervised Variable Selection.

A quick start

library(varPro)

data(BostonHousing, package = "mlbench")

## default call

o <- uvarpro(BostonHousing)

print(importance(o))

mean std z

nox 0.5880322 0.3838791 1.5318162

indus 0.4964445 0.3893825 1.2749533

rad 0.4051130 0.3518696 1.1513157

zn 0.4124063 0.4104604 1.0047407

medv 0.3700886 0.4275897 0.8655226

tax 0.2813970 0.3510989 0.8014749

crim 0.2791197 0.3866170 0.7219540

dis 0.2617584 0.3878109 0.6749641

lstat 0.2666589 0.3990492 0.6682358

ptratio 0.2297203 0.3440373 0.6677192

rm 0.2032958 0.3678408 0.5526733

age 0.1778247 0.3459164 0.5140685

b 0.0000000 0.0000000 NaN

chas 0.0000000 0.0000000 NaN

## unsupervised splitting

o <- uvarpro(BostonHousing, method = "unsupv")

print(importance(o))

mean std z

nox 0.4869640 0.3995163 1.2188839

indus 0.4495944 0.4044867 1.1115182

lstat 0.4240813 0.4392637 0.9654369

crim 0.3803382 0.3983700 0.9547361

dis 0.3802262 0.4123258 0.9221499

tax 0.3220476 0.3811110 0.8450231

ptratio 0.3191808 0.3920556 0.8141211

medv 0.3302492 0.4193045 0.7876120

rm 0.3270985 0.4244647 0.7706141

rad 0.2503864 0.3309411 0.7565889

age 0.3014338 0.4085133 0.7378802

chas 0.2578039 0.3717827 0.6934263

zn 0.2466710 0.3703855 0.6659845

b 0.0000000 0.0000000 NaNExample with Factors

## load the data

data(BostonHousing, package = "mlbench")

## convert some of the features to factors

Boston <- BostonHousing

Boston$zn <- factor(Boston$zn)

Boston$chas <- factor(Boston$chas)

Boston$lstat <- factor(round(0.2 * Boston$lstat))

Boston$nox <- factor(round(20 * Boston$nox))

Boston$rm <- factor(round(Boston$rm))

## call unsupervised varpro and print importance

print(importance(o <- uvarpro(Boston)))

mean std z

indus 0.54117940 0.3271978 1.6539825

rm6 0.56326599 0.3975106 1.4169835

zn0 0.51511629 0.3794794 1.3574289

rad 0.36567070 0.3642130 1.0040022

tax 0.26527079 0.3446583 0.7696632

dis 0.28795676 0.3760424 0.7657561

lstat1 0.25008573 0.3660272 0.6832436

medv 0.24229301 0.3756820 0.6449418

ptratio 0.18427676 0.3168359 0.5816159

crim 0.18407113 0.3258101 0.5649645

nox8 0.17606129 0.3185826 0.5526393

nox11 0.11161593 0.2519212 0.4430588

nox9 0.08109181 0.2257001 0.3592901

nox12 0.06632392 0.1892204 0.3505114

nox10 0.07201069 0.2107668 0.3416604

nox17 0.06073111 0.1777529 0.3416604

age 0.00000000 0.0000000 NaN

chas 0.00000000 0.0000000 NaN

lstat0 0.00000000 0.0000000 NaN

lstat2 0.00000000 0.0000000 NaN

lstat3 0.00000000 0.0000000 NaN

lstat6 0.00000000 0.0000000 NaN

nox13 0.00000000 0.0000000 NaN

nox14 0.00000000 0.0000000 NaN

rm5 0.00000000 0.0000000 NaN

rm7 0.00000000 0.0000000 NaN

rm8 0.00000000 0.0000000 NaN

zn12.5 0.00000000 0.0000000 NaN

zn20 0.00000000 0.0000000 NaN

zn28 0.00000000 0.0000000 NaN

zn75 0.00000000 0.0000000 NaN

## get top variables

get.topvars(o)

[1] "indus" "rm6" "zn0" "rad" "tax" "dis" "lstat1" "medv"

[9] "ptratio" "crim" "nox8" "nox11" "nox9" "nox12" "nox10" "nox17"

[17] "age" "chas" "lstat0" "lstat2" "lstat3" "lstat6" "nox13" "nox14"

[25] "rm5" "rm7" "rm8" "zn12.5" "zn20" "zn28" "zn75"

## map importance values back to original features

print(get.orgvimp(o))

variable z

3 indus 1.6539825

6 rm 1.4169835

2 zn 1.3574289

9 rad 1.0040022

10 tax 0.7696632

8 dis 0.7657561

12 lstat 0.6832436

13 medv 0.6449418

11 ptratio 0.5816159

1 crim 0.5649645

5 nox 0.5526393

4 chas 0.0000000

7 age 0.0000000

## same as above ... but for all variables

print(get.orgvimp(o, pretty = FALSE))

crim zn indus chas nox rm age dis rad

0.5649645 1.3574289 1.6539825 0.0000000 0.5526393 1.4169835 0.0000000 0.7657561 1.0040022

tax ptratio b lstat medv

0.7696632 0.5816159 0.0000000 0.6832436 0.6449418 Custom Importance Functions – Option 1: Inline Entropy

VarPro allows users to define a custom importance function through

the (hidden) entropy argument. This function is evaluated

internally during forest construction.

The custom function must return a list with two elements: 1. A scalar

importance value. 2. An entropy list containing the

comp and oob membership vectors.

Example:

my.entropy <- function(xC, xO, ...) {

wss <- mean(apply(rbind(xO, xC), 2, sd, na.rm = TRUE))

bss <- mean(apply(xO, 2, sd, na.rm = TRUE)) +

mean(apply(xC, 2, sd, na.rm = TRUE))

imp <- 0.5 * bss / wss

entropy <- list(comp = list(...)$compMembership,

oob = list(...)$oobMembership)

list(imp = imp, entropy)

}

o <- uvarpro(BostonHousing, entropy = my.entropy)

print(importance(o))

mean std z

nox 0.5689125 0.3900506 1.4585608

indus 0.5087139 0.3900071 1.3043709

rad 0.3504640 0.3520091 0.9956106

zn 0.3997953 0.4147441 0.9639565

medv 0.4126304 0.4310544 0.9572582

tax 0.3490256 0.3727909 0.9362502

crim 0.3446691 0.3990397 0.8637464

dis 0.2564835 0.3807887 0.6735587

ptratio 0.2151499 0.3324902 0.6470863

lstat 0.2429619 0.3907914 0.6217177

age 0.2182291 0.3743837 0.5829022

rm 0.1556733 0.3331967 0.4672112

b 0.0000000 0.0000000 NaN

chas 0.0000000 0.0000000 NaNCustom Importance Functions – Option 2: Post-hoc Construction

As an alternative, users can compute variable importance

after model fitting by working directly with the

$entropy output. This approach gives full control over the

definition of importance scores.

data(BostonHousing, package = "mlbench")

o <- uvarpro(BostonHousing[-(1:5), ])

beta <- get.beta.entropy(o)

print(beta[1:5, 1:5])

crim zn indus nox rm

crim 0.0000000000 0.10040957 1.0045794 3.79113503 0.2526244

zn 0.2941171442 0.00000000 1.2070505 11.04463518 0.8142999

indus 0.3386272960 1.13606934 0.0000000 7.88050758 1.3338613

nox 0.9156186492 0.64743152 1.5504832 0.00000000 0.9111166

rm 0.0001214442 0.05192334 0.1060687 0.02870288 0.0000000

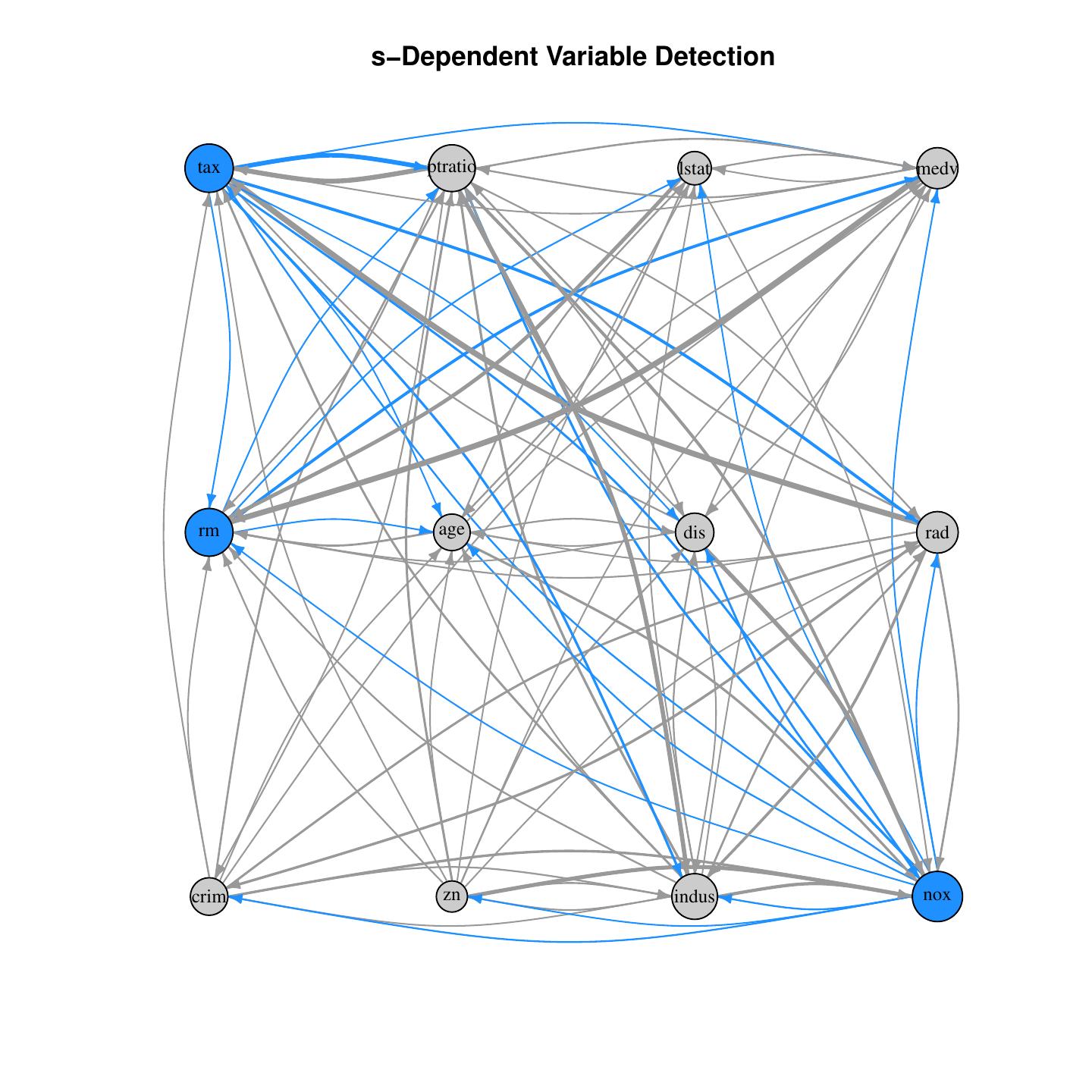

sdependent(beta)

In the above example of function get.beta.entropy, the

th

row serves as a ensembled regression model, representing the importance

scores for the

th

variable. The function sdependent provides S-dependence map

of the L1-logistic coefficient matrix — reveals variable dependence

structure without labels.

For large datasets, consider using parallel::mclapply to

improve computation time.

| Summary |

| Both approaches offer flexibility in defining importance scores tailored to domain-specific objectives. Option 1 is more integrated, while Option 2 offers full post-processing control. |

Cite this vignette as

M. Lu, L. Zhou, A.

Shear, U. B. Kogalur, and H. Ishwaran. 2024. “varPro: variable selection

for unsupervised problems vignette.” http://www.varprotools.org/articles/unsupervise.html.

@misc{HemantUvarpro,

author = "Min Lu and Lili Zhou and Aster Shear and Udaya B. Kogalur and Hemant Ishwaran",

title = {{varPro}: variable selection for unsupervised problems vignette},

year = {2024},

url = {http://www.varprotools.org/articles/unsupervise.html},

howpublished = "\url{http://www.varprotools.org/articles/unsupervise.html}",

note = "[accessed date]"

}